Table of contents

Table of contents

For large, multi-national companies with various locations or subsidiaries, achieving real-time liquidity visibility is a significant challenge. When funds are dispersed across numerous global bank accounts, gaining a clear, unified view of your cash position is nearly impossible—a situation that hinders effective resource allocation and drives up borrowing costs.

Challenges like these are why 83% of large businesses pool their cash at a regional or global level. With cash pooling, you create a centralized master account to hold all of your business’s funds, either physically or virtually. Benefits can include higher potential interest earnings, reduced external borrowing, and enhanced cash flow transparency.

That said, cash pooling also creates significant accounting complexity. It requires accounting teams to manage high-volume intercompany loans, perform detailed interest calculations, execute necessary eliminations for consolidation, and ensure rigorous transfer-pricing compliance on intercompany rates.

In this article, we’ll explain the different types of cash pooling, offer tips on navigating risks and challenges, and show how Intuit Enterprise Suite can help your business implement cash pooling.

How does cash pooling work?

Cash pooling is a liquidity management strategy that aggregates a company’s various bank account balances into a single master account. Often used by large businesses and multi-entity enterprises, cash pooling offers greater control over cash resources, improving liquidity, and maximizing interest earnings.

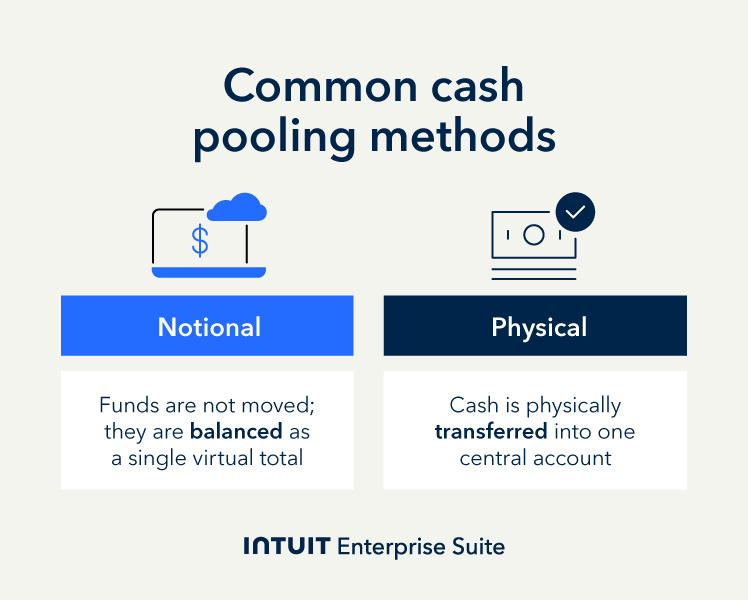

There are two main cash pooling methods:

- Notional pooling: funds in multiple accounts are treated as one virtual balance

- Physical pooling: cash is physically transferred into a central cash account

As a financial leader, you’ll need to review your business structure as well as regional regulations to determine which cash pooling option is best.

Why should you practice cash pooling?

Cash pooling provides multiple advantages for mid-size or large enterprises—including significant cost savings.

A study by Citibank found that large companies ($1 billion to $5 billion in revenue) saw a 23% higher return on invested capital (ROIC) and a 27% higher return on equity (ROE) when pooling cash.

Here are some other advantages and disadvantages of using cash pooling:

Let’s say you own a large retail business with store locations, warehouses, and distribution centers scattered across the country. With cash pooling, your borrowing costs are reduced (by netting balances), and any surplus cash you carry earns higher interest because balances are concentrated in a single master account for liquidity optimization.

Types of cash pools

There are two main types of cash pooling you can implement: notional and physical.

The first involves using one central account to virtually hold money, while the second method involves physically transferring cash from subsidiary accounts into a master account.

Let’s explore how each method works in more detail.

What is notional pooling?

Notional pooling is when balances from multiple accounts are recorded as a net balance for one centralized account. This results in the various cash balances being treated as one single balance, without the need to physically move money. In fact, the bank accounts involved remain legally separate.

For accounting purposes, this form of cash pooling creates a complex, but purely virtual, web of intercompany loan balances and interest accruals. And even though money isn’t actually moved, loans and interest must be tracked and recorded for internal management, transfer pricing, and tax compliance purposes.

Example: ABC Tool Manufacturing has three subsidiaries, each with its own bank account, located in the US ($20,000), Brazil ($14,000), and China ($17,000). Because China does not allow physical pooling, notional cash pooling is used. The company opens a central bank account with a global bank that is able to virtually aggregate the balances. ABC Tool Manufacturing will now earn higher interest rates on their $51,000 balance.

What is physical pooling?

Physical pooling is the process of transferring cash balances to a single central concentration account. Surplus cash from subsidiaries is transferred or swept into the master account on a daily, weekly, or monthly basis. And any deficiencies are covered by sweeping funds out of the account.

When it comes to accounting, this pooling method can result in a high volume of daily journal entries recording intercompany due-to/due-from balances for each sweep. On the upside, this physical movement of funds can create a clear audit trail for regulatory compliance.

Example: Construction Bros has four subsidiary brands in the Southern, Northeastern, Western, and Midwestern regions of the US. The Southern location has $10,000, the Northeastern location has $15,000, the Western location has $25,000, and the Midwestern brand has a deficit of $5,000.

The construction company sets up a central bank account with automatic weekly transfers. At the end of the week, the new account shows a balance of $50,000. Now Construction Bros can transfer $5,000 from the master account to cover the Midwestern shortfall.

Why is cash pooling an accounting challenge?

While there are many benefits to cash pooling, the practice can create several challenges for your accounting team. The main cause of these issues is the disconnect between the treasury function that establishes the pool and the accounting team that records the results.

The result of this disconnect can create recordkeeping issues, raise tax concerns, and introduce compliance risks.

High-volume intercompany loans

Both physical and notional cash pooling methods create complex, high-volume intercompany lending that your accounting system must manage. According to a study by BlackLine, 99% of large multinational companies face challenges managing their intercompany financial processes.

Issues include: recording daily interest income and expense allocations, managing constant fluctuations in intercompany due-to/due-from balances, and reconciling discrepancies in timing for when movements are recorded and currency.

Navigating these challenges requires a robust accounting software or enterprise resource planning (ERP) system. Manual recording and spreadsheets can lead to significant errors and inconsistencies. With software in place, eliminations can be automated, subsidiary relationships can be easily tracked, and compliance with accounting standards like generally accepted accounting principles (GAAP) can be maintained.

Manual reconciliation can lead to data inconsistencies, which can delay closing processes, produce inaccurate financial statements, and create tax and regulatory issues.

Transfer pricing

The biggest accounting challenge in transfer pricing is the “arm’s length” principle, which requires that intercompany transactions must be priced as though they occurred between two independent, unrelated entities acting solely in their own economic interest.

So, when one subsidiary lends to or borrows from another via the pool, the interest charged must be at an "arm's length" rate to comply with transfer pricing rules.

To determine arm’s length pricing, you’ll need to find comparable transactions, determine how the economic benefit should be allocated, evaluate credit ratings, and review current market conditions. For example, suppose Subsidiary A takes out a $50,000 loan from a third-party lender at 8.5%. In that case, you must charge the same 8.5% on a $50,000 intercompany loan for that subsidiary without discounting or preferential terms.

Tax risks

Cash pooling can create additional tax and regulatory compliance risks, especially for cross-border transactions.

Some of the key risks to monitor include:

- Transfer pricing issues: When interest rates are deemed inappropriate, tax authorities can impose penalties. Timely reporting of intercompany balances and interest calculations is essential for compliance.

- Recharacterization of balances: If tax authorities reclassify your short-term loans as long-term ones or as equity contributions or constructive dividends, you may face significant tax adjustments, such as loss of deductions and penalties. Clear documentation, avoiding permanent loans, and regular reviews of cash pool activity help prevent this.

- Tax withholding issues: Cross-border transactions can lead to increased withholding obligations. You’ll need to review double taxation treaties and maintain accurate records to qualify for tax relief.

- Prohibited cash pooling: In some countries, cash pooling is heavily restricted or completely prohibited. To avoid legal consequences, you may need to consider alternatives like in-house banking or cash concentration.

The cash pooling implementation checklist

Once you’ve decided to use cash pooling to centralize liquidity and picked the method that's the best fit for your enterprise, it’s time to properly set up and configure your account.

Here is a quick checklist of steps you can take to ensure a smooth transition:

For a practical example, consider the hypothetical construction group, The Building Guys. This company operates three key units: Infrastructure Depot, Housing Heroes, and EquipLease.

To establish cash pooling across all three units, they will follow these steps:

1. Draft legal agreements: The Building Guys draft a Master Pooling Agreement that legally binds all three companies to the pool's rules and interest rates.

2. Standardize the Chart of Accounts (COA): The treasury team ensures all subsidiaries use the same COA codes to record internal loans and interest activity.

3. Set up intercompany relationships in your accounting software: The software is configured so that when a subsidiary borrows cash, it is recorded as a "customer" of the central pool, tracking the internal debt.

4. Choose a bank and set up a master account: A single commercial bank is selected, and the master concentration account is established to hold all the group's pooled surplus cash.

5. Define target balances for each account in the pool: Management sets Infrastructure Depot to maintain a $50,000 minimum and EquipLease to a zero balance account (ZBA)target.

6. Set up automatic sweeps to move funds between accounts: The bank is instructed to run nightly sweeps to pull all excess cash above target balances into the master account.

7. Pre-configure journal entry templates: Templates are created to automatically calculate and post interest charges on internal loans, ensuring tax compliance.

8. Set up regular reports to provide a consolidated view of the group's cash position: The CFO receives a daily Cash Summary Report showing the total cash available and the net internal position of all three subsidiaries.

It’s important to regularly monitor your cash pooling’s performance and adjust as needed to help preserve subsidiary autonomy and ensure regulatory compliance.

With a tool like Intuit Enterprise Suite, you can manage all your data in one place, preventing a disconnect between your treasurer and accounting team.

How Intuit Enterprise Suite supports cash pooling

To effectively implement cash pooling, you require more than just an accounting system—you need an ERP-grade, AI-powered multi-entity platform. This robust system must be built to handle the massive transaction volume, complex international tax rules, and rigorous compliance requirements inherent in a global cash pooling structure.

Intuit Enterprise Suite offers robust tools to help you navigate the cash pooling process:

- Automated eliminations: The software automatically identifies and eliminates intercompany transactions, producing fast, accurate financial statements.

- Multidimensional accounting: You can tag transactions by entity or department, simplifying the allocation of interest income and expenses.

- Audit trail: With all transactions tracked, audits can become more efficient.

- Compliance: The system can help support compliance with all regulations, such as GAAP or international financial reporting standards (IFRS).

Our platform has an estimated 299% ROI within the first three years of adoption. Whether you manage thousands of daily transactions, need to adhere to local regulations, or are working to align financial and accounting teams, Intuit Enterprise Suite provides the foundation your cash pooling structure requires.

Boost productivity and enhance profitability

Cash pooling can offer you the flexibility to move funds across subsidiaries quickly and provide you with real-time insight into your liquidity. However, cash pooling, whether or notional or physical, does come with challenges. To overcome obstacles like reconciling intercompany transactions and tax compliance, Intuit Enterprise is here to help.

Our automation, AI, and compliance tools are specifically designed to address these pressures. We help manage the high volume of daily intercompany entries, ensure alignment between treasury and accounting, and generate audit-ready reporting required for a successful cash pooling deployment.

Whether you need a full-featured accounting solution or a system that integrates with your existing ERP system, the Intuit Enterprise Suite can support your implementation.

Check out upcoming events and learn more about Intuit Enterprise Suite.

Customer stories

Case study

How FEFA Financial scaled up with Intuit Enterprise Suite (No ERP migration needed)

Case study

Case study: Fire & Ice transforms multi-entity challenges with Intuit Enterprise

October 25, 2024

Case study

Four Points RV Resorts review: Why they chose Intuit Enterprise Suite over NetSuite

October 25, 2024

Construction

Migrating to Intuit Enterprise Suite took 2 hours (with zero disruption) for this aspiring $50M revenue business

April 25, 2025

Case study

Humble House Foods case study: How they improved visibility & simplicity using Intuit Enterprise Suite

September 24, 2025

More product updates

Product update

What’s new in Intuit Enterprise Suite spring 2025

April 1, 2025

Product update

Intuit Enterprise Suite 2025 update: AI agents & automation enhancements

July 22, 2025

Product update

What’s new in Intuit Enterprise Suite November 2025: The AI-native ERP that adapts with your business

November 14, 2025