Today’s high school students handle more financial complexity than previous generations, juggling digital banking, investment apps, student loan decisions, and new payment technologies. This creates valuable opportunities for early financial education to make a lasting impact.

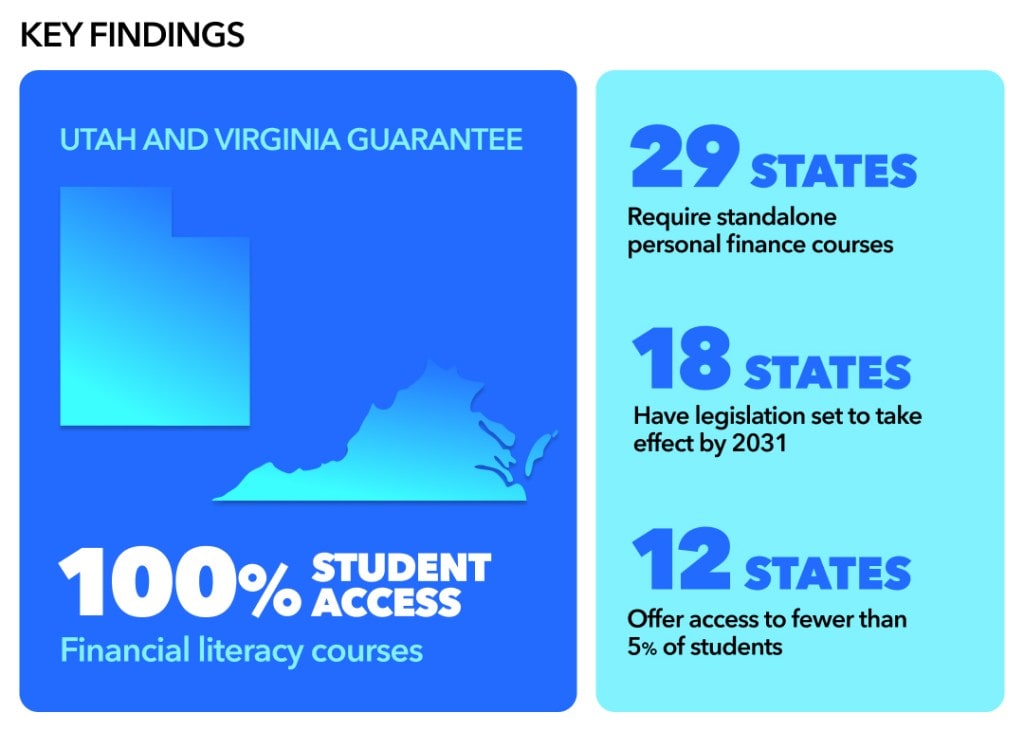

States across the country are responding by expanding access to financial literacy programs. As of August 2025, 29 states guarantee a standalone personal finance course for all public high school students.

More states continue to guarantee that public high school students will take a personal finance course before graduation, representing significant progress in ensuring students receive structured financial education before adulthood. Additional states are advancing similar legislation, demonstrating a widespread commitment to equipping young people with essential money management skills.

As high school administrators integrate these programs and teachers adapt their curricula, students nationwide gain earlier access to money management fundamentals that can serve them throughout their entire lives.

Intuit analyzed publicly available data across all 50 states, examining graduation requirements, course accessibility, youth employment opportunities, math proficiency levels, and policy implementation strength. Rather than simply ranking performance, this analysis reveals which states are pioneering financial literacy requirements and identifies the most significant opportunities for continued growth.

This perspective helps educators, parents, and administrators understand where momentum is building and where the next wave of progress might emerge.

Key Findings

- Standalone course requirements drive success: All top 10 performing states require dedicated personal finance courses for graduation, demonstrating the power of comprehensive, focused financial education over integrated approaches.

- Legislative momentum creates a promising pipeline: 18 states have legislation scheduled to take effect between 2025 and 2031, potentially reshaping the national picture as these policies roll out over the next several years.

- Recent implementations show immediate impact: Five states that implemented new requirements between 2020 and 2024—including Nebraska (no. 3) and Rhode Island (no. 4)—landed in the top tier of performers, suggesting swift policy benefits.

- Significant opportunity exists in major population centers: In 12 states, fewer than 5% of high school students currently have access to financial literacy education, highlighting a significant opportunity to expand access and empower more young people nationwide,

- Perfect access is achievable: Utah and Virginia demonstrate that 100% student access to financial literacy courses is attainable and highly effective, providing a clear model for other states to follow.

Overall State Rankings

States received scores out of 18 possible points based on graduation requirements, student access to personal finance courses, and supporting factors like youth employment rates and test scores. When states tied on overall scores, the percentage of students guaranteed to complete personal finance coursework determined final rankings.

States Leading the Way

Utah, Wisconsin, and Nebraska earned top rankings through exceptional student access, robust graduation requirements, and strong youth employment opportunities that enable students to apply their learning immediately. These states demonstrate that comprehensive financial literacy education is achievable and highly effective when implemented strategically.

As Dr. Stepan Mekhitarian, K-12 Outreach National Manager at Intuit, explains:

“Developing personal finance standards at the elementary and middle school levels, in addition to high school, is a key best practice to ensure learning continuity and the development of a healthy money mindset from an early age, especially as students begin to make monetary decisions earlier and earlier.”

These insights reinforce why leading states stand out: they not only require personal finance instruction but also create systems that engage students early and often—building both foundational understanding and long-term habits.

Utah

Score: 17.1

Utah requires a standalone personal finance course for graduation and achieves 100% student access across public high schools. In 2008, the state was the first to implement this requirement, providing more than 15 years of operational data. Utah maintains a 63% youth employment rate, the highest among top-performing states.

The state’s top ranking reflects this combination of universal access, long-term implementation experience, and high youth employment opportunities. Utah’s graduation requirement ensures comprehensive coverage, while its employment rate provides practical application opportunities for classroom learning.

Wisconsin

Score: 15.9

Wisconsin mandates standalone personal finance coursework for graduation, with implementation scheduled for the class of 2028. Current student access reaches 44% of public high school students. The state maintains a 58% youth employment rate among high school-aged students—one of the highest rates in the country.

Wisconsin’s no. 2 ranking demonstrates strong performance during the pre-implementation phase. The state’s graduation requirements are established, and current access levels exceed national averages. The 2028 implementation timeline positions Wisconsin for potential access rate improvements in future assessments.

Nebraska

Score: 15.0

Nebraska implemented its standalone personal finance graduation requirement in 2021. The state achieves 86.8% student access and maintains a 61% youth employment rate. Nebraska’s implementation represents recent policy adoption with measurable current outcomes.

The state’s no. 3 ranking reflects this recent implementation success. Nebraska’s access rate places it among the highest nationally, while its youth employment rate provides practical learning opportunities. The 2021 implementation date demonstrates relatively rapid policy-to-outcome results. These three states demonstrate different implementation timelines—established (Utah), upcoming (Wisconsin), and recent (Nebraska)—while maintaining common policy foundations: standalone graduation requirements, substantial student access, and strong youth employment rates above 44%.

Where There’s Opportunity for Growth

California, Nevada, and Delaware currently rank among states with the most room for growth in financial literacy education. Each state shows different baseline conditions and policy approaches, offering insights into different pathways for expanding student access to comprehensive financial education.

California

Score: 0.9

California currently maintains limited state-level financial literacy requirements, with 0.8% of students having access to personal finance courses. Youth employment levels reach 24%, which is the lowest in the country (tied with Nevada).

Although the state ranks no. 50 nationally, California is taking steps to improve financial literacy access in high schools. It established a 2031 implementation timeline for enhanced financial literacy standards. This extended window creates space for comprehensive planning and resource development. Given the size of California’s student population—nearly 6 million—even incremental improvements could lead to meaningful outcomes at scale.

Nevada

Score: 3.0

While Nevada currently requires high schools to offer financial literacy coursework, not all students are required to take classes where financial literacy concepts are taught. Only 4.2% of students are guaranteed access. The state ranks no. 49 nationally, with youth employment at 24% among high school students.

Nevada’s existing course infrastructure creates a strong foundation for future growth. With offerings already in place, the state is well-positioned to increase student participation rates through thoughtful policy updates.

The gap between course availability and student access represents Nevada’s primary growth opportunity. Transitioning from “required to be offered” to “required to be taken” could significantly improve student access rates.

Delaware

Score: 3.3

Delaware implements financial literacy standards through district-level requirements and achieves 6% student access to personal finance courses. While the state ranks no. 48 nationally, it maintains a youth employment rate of 49%, the highest among these three states.

Delaware’s district-based approach provides flexibility for local implementation while creating opportunities for more standardized statewide requirements. The state’s relatively high youth employment rate offers a foundation for practical application of financial concepts.

Although Delaware’s access rate is currently limited, its existing infrastructure creates room for growth. With increased coordination at the state level, the state has the potential to expand student access and deliver more consistent financial education across districts.

These states demonstrate different starting points for financial literacy expansion, from limited requirements (California) to district-based standards (Delaware). Each state’s current infrastructure and timeline reflect the capacity for meaningful growth in delivering comprehensive financial education to more students.

Although these states ranked the lowest, they have opportunities to make headway without complete overnight overhauls. As Mekhitarian explains, “For states that haven’t yet adopted financial literacy standards, the most realistic first step is to establish them—ideally spanning K–12, rather than just high school. From there, requiring a standalone personal finance course can ensure every student gains consistent, meaningful exposure.”

He adds, “Even small steps can make a difference. States that are just beginning can start by developing financial literacy lesson playlists for use in advisory periods or freshman seminars. Over time, those efforts can build toward full K–12 standards and eventually standalone courses.”

How We Measured Financial Literacy Readiness

To evaluate how well each state prepares high school students for real-world financial decision-making, we analyzed six key factors across all 50 states representing access, policy strength, and student outcomes. Each factor was scored on a scale of 0–3 and then weighted based on its importance. The total possible score was 18.

Metrics and Weighting

- Graduation Requirement (25%): Whether personal finance is a mandated, standalone course for all students.

- Student Access to Courses (25%): The percentage of students guaranteed at least one semester of personal finance instruction.

- Student Financial Literacy Scores (15%): State-level test results and survey data capturing what students actually know about money management.

- Youth Employment Rate (15%): A proxy for hands-on financial experience gained through part-time work.

- Academic Proxy – Grade 8 Math (15%): Early numeracy skills that form the foundation for financial literacy.

- Policy Implementation Timeline (5%): How long financial literacy policies have been in place, signaling maturity and stability.

Ranking and Tiebreakers

States were ranked based on their weighted total score. In the event of a tie, we used the percentage of high school students guaranteed to take a personal finance course by 2025 as the tiebreaker.

This methodology ensures our rankings reflect not only policy but also the real-world access and preparedness of students across the US.

Bring Financial Literacy to Every Classroom for Free

Empowering the next generation with financial knowledge goes far beyond rankings. Every student deserves the confidence to make informed money decisions, and educators need resources and tips to teach personal finance to bring those lessons to life.

Intuit for Education is a free financial literacy curriculum for high school and college students. Students learn real-world skills like budgeting, saving, and managing credit through interactive modules and simulations featuring familiar tools like TurboTax, QuickBooks, and Credit Karma. The program also offers free, comprehensive financial literacy resources that teachers, parents, and administrators can use to help implement and teach the curriculum.

Bringing financial literacy to every classroom is simpler than ever. Intuit’s financial literacy resources, like the Hour of Finance program, self-paced personal finance curriculum, and guided personal finance curriculum, give students access to financial literacy tips and tricks that help them build a foundation for lifelong financial confidence.